Material Insight: The Dielectric Constant of PCB Materials

Material Insight: The Dielectric Constant of PCB Materials American Made Advocacy: What About the Rest of the Technology Stack?

American Made Advocacy: What About the Rest of the Technology Stack? It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring Habits

It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring HabitsCommercial Demand Continues to Be the Main Driver of Personal Computing Device Shipments into the GCC Region

March 26, 2024 | IDCEstimated reading time: 1 minute

The Gulf Cooperation Council (GCC) personal computing device (PCD) market, which is made up of desktops, notebooks, and workstations, declined 4.0% year on year in 2023, with high inventory levels and reduced consumer spending the primary causes. That's according to the latest industry analysis conducted by International Data Corporation (IDC), with the firm's newly updated Worldwide Quarterly PCD Tracker showing that shipments across the region totaled 3.54 million units in 2023.

The six markets that make up the GCC — Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE — witnessed varied performances in 2023. Oman and Kuwait were the only markets to see year-on-year growth (17.8% and 3.9%, respectively), with the remainder all experiencing declines. However, it is important to note that Saudi Arabia and the UAE together account for 80% share of the GCC market.

"Digital adoption among businesses and governments is proliferating across the GCC, and consumers are continuing to enjoy enhanced experiences via digital solutions," says Isaac T. Ngatia, a Dubai-based senior analyst at IDC. "This has led to a higher base of users, which vendors have been trying to capture. However, the wallet share for devices among consumers has been under pressure as purchases made during the COVID era continue to linger on. The commercial segment has therefore been the bright spot for pushing devices into the market, and this will continue to be the case throughout 2024."

The product mix has witnessed an increase in the volume of desktops (towers and all-in-one), with 2023 shipments of these devices comparable to pre-COVID levels. The year closed with desktops accounting for 30.9% of PCD shipments to the region, the highest since the 31.7% share seen in 2019. This increase in desktop shipments can be attributed to back-to-office initiatives and increased demand among learning institutions and government offices, as well as to general device refresh cycles.

In the final quarter of the year (Q4 2023), the overall PCD market witnessed significant growth across the region, with shipments up 8.4% year on year. The fulfilment of existing contracts and shipments to cater for end-of-year fulfilments were the key factors driving this growth.

Looking ahead, IDC expects the GCC PCD market to remain relatively flat in 2024. Shipments into the commercial segment will increase 3.7% year on year; however, consumer-focused shipments will decline by 6.8%, with this segment seeing only regular device replacements throughout the year.

Share on:

Suggested Items

Avnet Launches QCS6490 Vision-AI Development Kit

05/17/2024 | AvnetThe QCS6490 Vision-AI Development Kit from Avnet enables engineering teams to rapidly prototype hardware, application software and AI enablement for multi-camera, high-performance, Edge AI-enabled custom embedded products.

Nortech Systems Reports Q1 Results and Actions to Reduce Facility Costs

05/17/2024 | BUSINESS WIRENortech Systems Incorporated, a leading provider of engineering and manufacturing solutions for complex electromedical and electromechanical products serving the medical, industrial and defense markets, reported first quarter ended March 31, 2024 financial results.

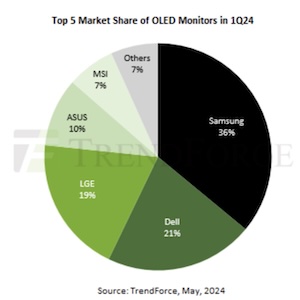

Shipments of OLED Monitors Hit 200,000 Units in 1Q24, Annual Forecast to Reach 1.34 Million

05/17/2024 | TrendForceTrendForce’s latest report reveals a robust start to 2024 for OLED monitors, with shipments reaching approximately 200,000 units in the first quarter—marking a YoY growth of 121%.

The ICAPE Group Reports Revenue for Q1 2024

05/16/2024 | ICAPE GroupThe ICAPE Group, a global technology distributor of printed circuit boards (PCB) and custom-made electromechanical parts, announced its revenue for the first quarter of 2024.

Sypris Reports Q1 2024 Results; Revenue Up 10%

05/15/2024 | Sypris Solutions Inc.The Company’s first quarter 2024 consolidated revenue increased 10.1% to $35.6 million compared with the prior-year quarter, representing the 11th quarter of double-digit year-over-year growth during the past 12 quarterly periods.